Letter to Investors

Dear Clients, Colleagues, and Friends of Greenwich Advisors:

This Fourth of July marks the 250th anniversary of American independence. We have much to celebrate, especially the freedoms and rights that have shaped our nation. I believe the Founding Fathers would be proud to see their pioneering spirit endure today through the entrepreneurial energy that continues to drive American innovation.

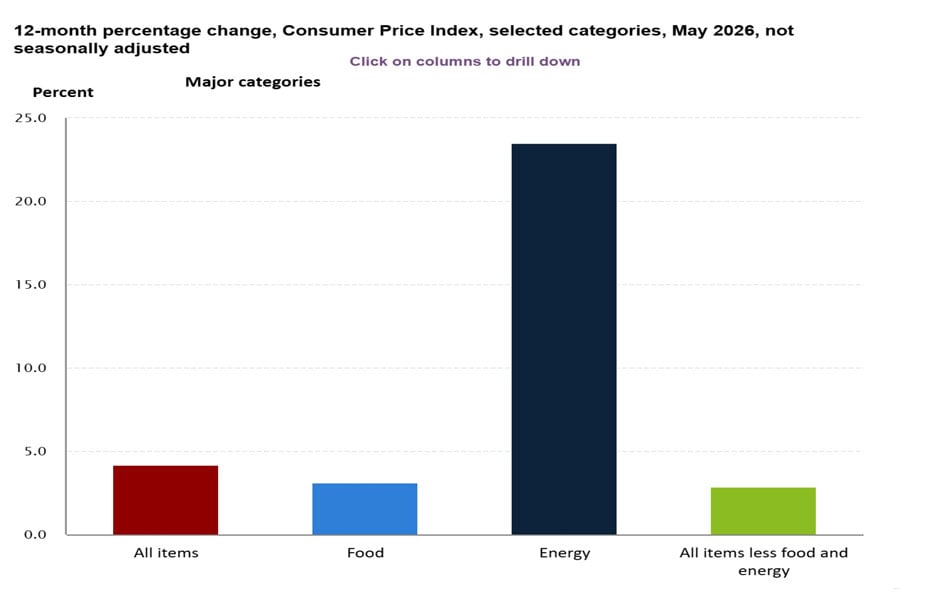

The first half of 2026 was shaped by optimism over artificial intelligence, tempered by geopolitical risk. Conflict in Iran pushed energy prices up 23.5% and overall inflation higher by 4.2%, as of May’s data (see figure 1), while the war in Ukraine continued to exact a heavy toll in lives and property. Expectations that a change in leadership at the Federal Reserve would quickly bring lower interest rates have also faded. Kevin Warsh’s first meeting as Chairman made clear that monetary policy remains in the hands of the voting members of the Federal Open Market Committee, which remains dedicated to its dual mandate of maximum employment and stable prices. As you can see below, prices are not stable.

Figure 1. 12-month CPI Source: U.S. Beureau of Labor Statistics

Market Returns

Stocks markets worldwide have performed well during the first half of the year. The S&P 500 index gained 10.2% year to date, while stocks in emerging markets continued to outperform. The MSCI EAFE index gained 9.4% and the MSCI Emerging Market index gained 23.9%. Rising inflation expectations and fading hopes of rate cuts caused bonds to underperform, including the Bloomberg Aggregate Bond index which returned a meager 0.6%, while 90 day US Treasury Bills earned 1.7%. On the back of the Iranian military conflict and the subsequent closing of the Straight of Hormuz, oil gained 21%. Bitcoin was the big loser, failing to live up to its store of value hype, declining 33.4%.

Alternative Investments: Illiquidity Is a Feature, Not a Flaw

Private credit has attracted critical press this year as funds limited investor withdrawals. These critiques often overlook the fact that private credit funds were never meant to allow daily, monthly or even quarterly liquidity of your entire investment, instead these funds were designed to provide access to illiquid loans for long periods of time in exchange for higher interest rates. Except for the benefits of diversification and regular rebalancing, there is no free lunch in this world, and investors shouldn’t expect to earn interest rates materially greater than US Treasury Bonds without giving up something. That trade-off is liquidity. So, if your time horizon is long and your risk tolerance is such that you can invest in an illiquid asset to earn a higher return, then don’t let short term media commentary incite you to sell your private investments.

SpaceX IPO

During the second quarter, SpaceX IPO’d at a price of $135, offering $75 billion in shares to investors, at a valuation of $1.77 trillion, making it the largest IPO in history. SpaceX has three primary segments, Space, Connectivity, and AI. The Space segment dominates launch, with reusable rockets amazingly accounted for 95% of SpaceX launches in 2025. The Connectivity segment, Starlink, the undisputed leader in satelite communication, has over 10.3 million subscribers, operates in over 164 countries. Starlink is profitable and growing. Finally, the AI segment consists of 550 million active subscribers of x.com and Grok, and operates data center and compute infrastructure which added Anthropic and Google as clients this year. At IPO, the company has less than $20 billion in sales, valuing the company a ratio of 94x 2025 revenue, an expensive valution implying a flawless degree of execution across multiple highly complex business segments. The current price appears to have already discounted much of the future growth.

Digital World vs. Physical World

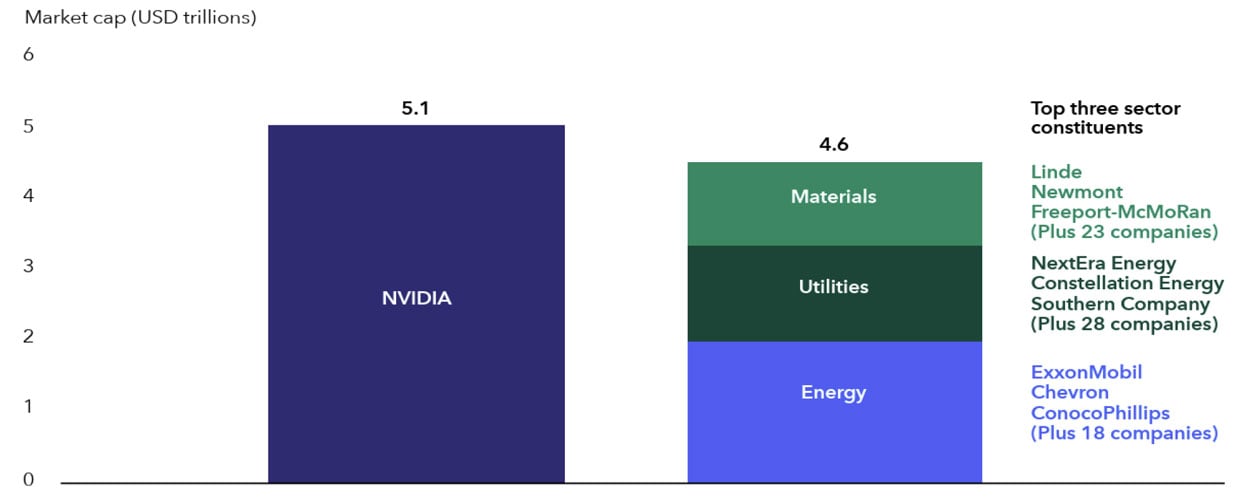

During times of unprecedented growth and investor optimism, valuations can get over-extended. There sometimes seems as if there is no limit to the optimism of wall street earnings expectations, and as a result, investors can inflate stock prices and their total market capitalization to incredible levels. That is exactly what we are seeing with Nvidia. I pose one question to you: if you had a spare $5.1 trillion laying around, would you rather own 100 percent of Nvidia or would you rather own 100 percent of the following (Exxon, Chevron, Conoco Phillips and the remaining 21 companies in the S&P 500 energy sector, plus Linde, Newmont Mining, & Freeport-McMoRan and the additional 26 companies in the S&P 500 materials sector, plus NextEra Energy, Constellation Energy, and Southern Company along with the additional 31 companies in the S&P 500 utilities sector) and have an extra $500 billion in cash left over? I would choose the physical world (see figure 2).

Figure 2. Digital World vs. Physical World, Sources: Capital Group, FactSet, RIMES, S&P Global. As of May 31, 2026.

Investing Outlook

The US economy has continued to defy the odds and the forecasts for recession growing around 2% with earning growth being extremely robust due to the spending on AI infrastructure. Even though earnings have been strong, stock prices have been even stronger, and valuations remain well above levels for us to be bullish. Technology stocks were the most overvalued and even though the recent correction there has brought valuations lower, 20X earnings for the S&P 500 based on forward 12-month estimates leave little room for disappointment and significant room for correction. On the other hand, we started the year bullish on energy shares, and we continue to be bullish energy. Global energy demand remains robust, global daily consumption of oil may exceed 105 million barrels of oil per day, and the global oil market has been deprived of over 1 trillion barrels. This leaves the world with dangerously low levels of inventory and extremely vulnerable to future supply shocks. Stay invested in energy shares including clean energy shares.

International equity markets continue to outperform, due to investors realizing the relative value with international companies trading at price to earnings ratios up to 30% cheaper than their US counterparts. Companies in Europe and Asia are using and deploying AI too, and everyone is reaping the productive benefits of these new technologies, including international companies.

Bonds are much more attractively priced today than they were in 2022 when the Federal Reserve started raising interest rates. Looking at the main bond market index, the Barclays Aggregate Bond Index, yields are now 4.6% compared to 1.75% then, giving investors a much larger yield cushion than before. There continues to be an important role for bonds in investor portfolios, providing a larger flow of interest income and giving investors an opportunity for appreciation if rates do go lower. With corporate bond spreads below 0.90%, investors are not paid sufficiently for the additional credit risk. Therefore, we believe that US Treasury Bonds and Municipal Bonds are more attractively priced.

There are no guarantees when investing. But, if you have a plan, focus on what you can control, diversify intelligently, rebalance diligently, manage emotions, and avoid market timing, you will improve your odds of success. If you have any questions, comments, or concerns, we would be delighted to talk to you. Thank you for the continued trust you have placed in us, and we wish you and those you care about a wonderful 250th Independence Day celebration!

Appreciatively,

Chris Tucker & Chris Kuehne