Brighter Days

If you are reading this, you are likely one of the lucky 6 billion on this planet who now reside in the middle or upper class, who have most basic needs met, have access to clean water, access to some electricity, and fuel for transportation. As this middle and upper class grows, so does the demand for energy to power our homes, the electronic gadgets, our Teslas, and to fuel the planes and cars for our family vacations. We all demand more energy, nearly 10 billion metric tons of oil equivalents per year at last count. As a result, there is an investment opportunity for those companies who can satisfy that demand with more affordable and cleaner energy, and the recent sell off in the share prices of energy companies has created an attractive opportunity for the long-term investor to buy.

Energy Demand is Growing

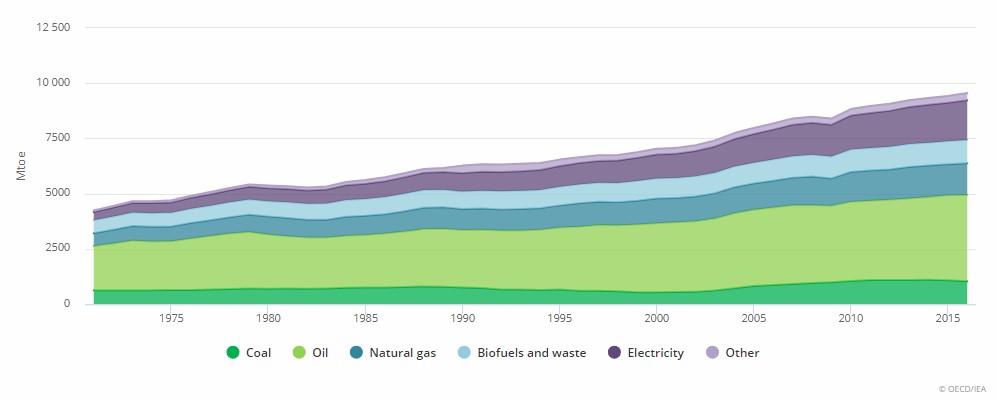

Total Worldwide Energy Consumption as measured by the International Energy Agency has risen from 4,661 Mtoe (million metric tons of oil equivalents) in 1973 to 9,555 Mtoe in 2016. Over the next twenty years if current trends persist, global population will grow 28% from 7 billion to 9 billion, and another 2.5 billion people join the middle and upper class, all of whom want to power up their homes, their vehicles, and take vacations. Clearly, we are going to need a lot more energy to brighten and to power this world.

World Energy Consumption in Mtoe

Valuations are attractive

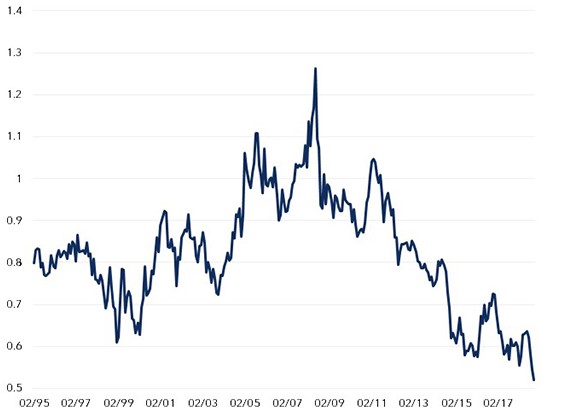

The weakness in the price of crude oil has put downward pressure on the share prices of energy companies. As of December 28, the S&P 500 Energy Sector has declined 19.98% vs. a decline of 7.25% for the S&P 500 Index. This decline in the share prices, has created valuations which are cheaper than historical averages and cheaper than the overall market. The Energy Sector’s Price to Earnings ratio now stands at 12.19x for this year’s estimate compared to 15.3x for the S&P 500 Index. Also, historical price to book valuations for the Energy Sector relative to the S&P 500 are some of the most attractive observed in the past 20 years.

Energy Sector Price to Book Relative to S&P 500

Source: BlackRock, Bloomberg

Fundamentals Remain Strong

With the energy price declines of 2015 still fresh in the minds of management, most of the major energy companies have been prudent with capital projects and are operating leaner, more cost-efficient companies. According to JP Morgan Research, analyst consensus forecast the industry profits to grow by 19.1% in 2019 and 10.7% in 2020. The two primary risks to the fundamental story is a trade war slows down the global economy or causes a recession. As a result, energy demand will be diminished. Short term supply imbalances in energy production could keep energy prices lower for longer. This negative narrative has contributed to the decline in share prices and created an investment opportunity for long term investors to buy attractively priced shares of energy companies.

Earnings estimates are likely to be reduced, but even so, the growth rates will likely still compare favorably to the overall economy and overall stock market. Cash flow and dividends are strong. The current dividend rate for Energy Select SPDR ETF, symbol XLE, is 2.96%, and for many individual companies we recommend, dividend yields range from 3.3% to 6.5%.

For investors focused on socially and economically responsible investing, the iShares Global Clean Energy ETF, symbol ICLN, invests in shares of companies that produce clean energy (wind, solar, etc.) and is also attractively priced with a Price to Earnings ratio of 13.9x, a Price to Book ratio of 1.3, and a trailing dividend yield of 2.4%.

Contact your financial advisor for a portfolio review and make sure your exposure to companies in the energy sector is appropriate for you, and feel free to contact us for more information on the high-quality energy companies we recommend for our investors seeking capital growth and dividend income.

D. Chris Tucker, CFA

Chief Investment Officer